A Majority of U.S. Adults Are Un- or Underinsured. It's Getting Worse.

New Survey Documents Deteriorating Health Care System

The Commonwealth Fund released the initial results of its biennial health insurance surveys today. Three data points suggest the majority of American adults aged 19-64 don’t have health insurance good enough to pay for the health care they need without going into debt or facing bankruptcy. All three metrics worsened over the past two years.

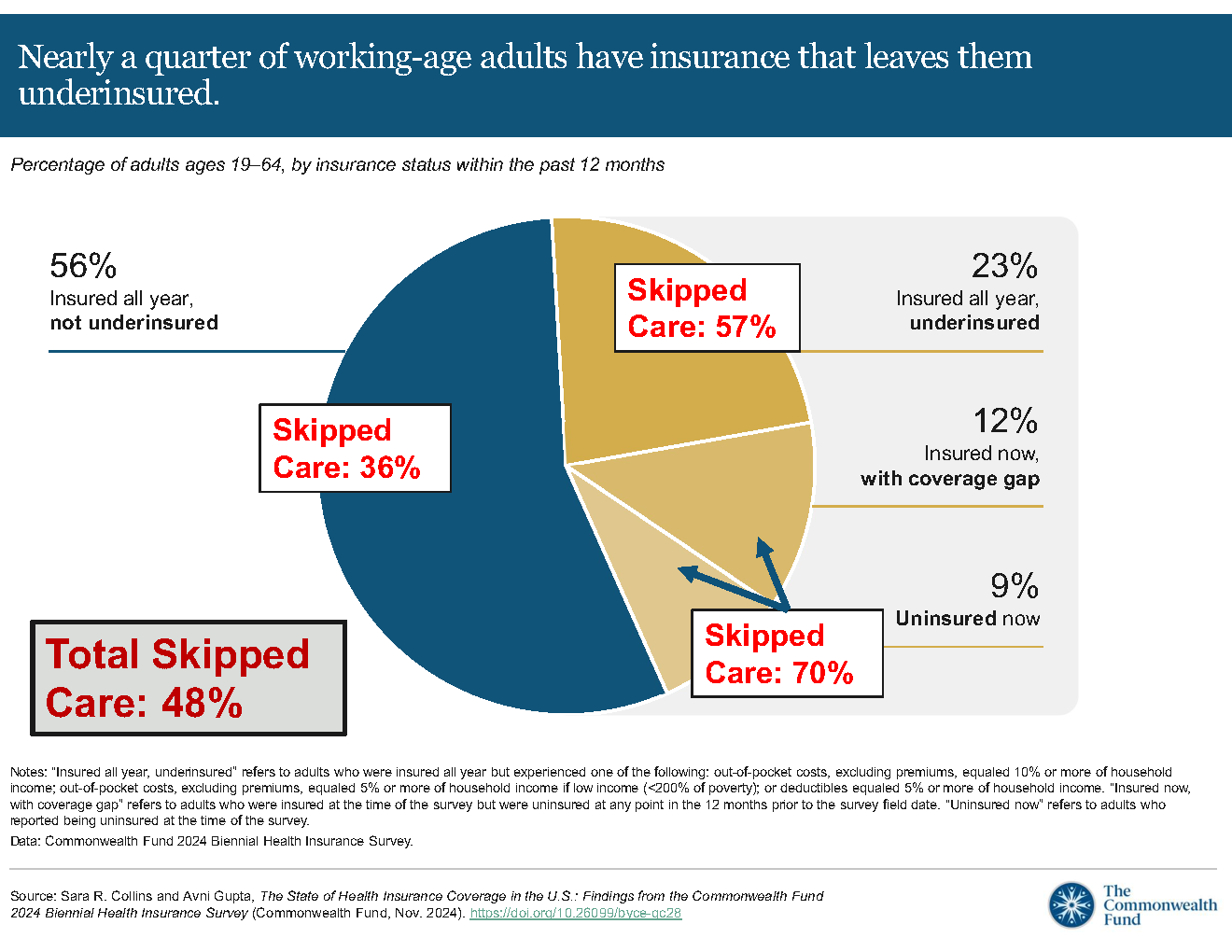

The percentage of adults aged 19-64 (“working age”) who skipped needed health care in the past year rose from 46% to 48% between 2022 to 2024.

A slight majority of working age adults had health insurance continuously for a full year that did not meet the Commonwealth Fund’s definition of being “underinsured,” although the percentage dropped from 57% to 56% over the past two years.

But even among these supposedly fully-insured adults, more than a third skipped needed health care because of cost, with the percentage growing from 32% to 36% since 2022, faster than other insurance categories.

The results paint a picture of a health care system incapable of delivering health care to most of the country’s adults despite extreme levels of spending. Nearly half of adults surveyed (48%) said that because of the cost of medical care, in the previous 12 months they: had a medical problem but did not visit a doctor or clinic; didn’t fill a prescription; didn’t get needed specialist care or; skipped a recommended test, treatment or follow up.

Those problems arose more frequently for people who had been uninsured at any time in the previous year or met the Commonwealth Fund’s technical threshold for underinsurance. Seventy percent of adults who had a period of uninsurance reported at least one of the four problems. Fifty-seven percent of people that the researchers define as “underinsured” skipped at least one of the four types of care.

Commonwealth defines someone as “underinsured” if they reported out of pocket costs of 10% or more of their household income, 5% or more in households earning less than 200% of the federal poverty level, or if their deductibles equaled 5% or more of household income regardless of actual spending. It’s almost certainly an undercount. Co-author Sara Collins confirmed in a background press briefing that the last part of the definition excludes copays, coinsurance and out of pocket maximums, while the entire process ignores the cost of premiums.

The most remarkable finding came among what we at Healing a Stealing call the “allegedly insured.” 36% of all adults who had insurance that Commonwealth’s researchers believe make them not underinsured told surveyors they had skipped medical care due to cost in the past year, up from 32% in 2022. Some portion of these people may have genuinely comprehensive coverage and skipped care due to unusual circumstances, but there’s no doubt that a more accurate definition of underinsured would include many of the allegedly well-insured.

The graphic below adds the responses to the questions on skipping care to the survey’s insurance categories - note that the researchers combined people who were uninsured at the time of the survey with those who reported a break in coverage earlier in the year when they reported results for skipping care.

The new survey results may help explain the disconnect between Vice President Kamala Harris’s policy expert supporters who insisted that the economy was good during the recent election campaign, and voters who told pollsters otherwise. They also make clear that policy changes likely to be pursued by the incoming Trump Administration will do nothing to fix a badly broken system.

Healing and Stealing alerted readers in March that the Democratic Party would rely on “a tsunami of fake good news” about health care for their 2024 campaign. They did exactly that.

In the debate and her economic plan, Vice President Harris said that the Affordable Care Act and her own personal leadership led to the lowest uninsurance rate in history, and “a record 21 million Americans” enrolled in ACA exchange coverage in 2024. The “record” ACA enrollment was driven in significant measure by the Great Medicaid Purge (details on Democratic proposals here and Medicaid here).

The Commonwealth Fund’s data also make clear that the uninsurance rate is largely meaningless given the dramatic increase in underinsurance since 2010, especially since costs force more than a third of allegedly well-insured adults to skip needed medical care. Even taking Commonwealth’s definitions at face value, the “record” ACA enrollment over the last two years coincided with a small actual decline in the percentage of allegedly well-insured U.S. adults, from 57% to 56%.

What matters is whether everyone has health insurance that pays for the health care they need. Commonwealth’s results from allegedly insured people coupled with the catastrophic levels of missed care for other categories show that the majority of American adults don’t.

People’s attitudes about their personal financial circumstances and broader economic trends are shaped by a wide variety of factors. But insisting that an “economy” leaving most adults to suffer illness and injury without treatment because they can’t afford to see a doctor, buy drugs or get tests, is “good” may not have demonstrated quite the level of empathy that national Democrats pride themselves on.

The data in the Commonwealth Fund surveys are an essential resource for anyone trying to understand the failures of the U.S. health care system. Few other organizations - if any - have invested the same level of resources and energy in documenting the rise of underinsurance in the U.S. The weaknesses in the definitions described above are not a failing - creating any metric from the cost-sharing provisions in the blizzard of different insurance “products” offered in the U.S. is a nightmarish task and deductibles are as good a proxy as any.

The report includes chilling documentation of the consequences of inadequate health insurance beyond skipping medical care. Twenty-nine percent of adults are paying off medical debt (including 21% of the allegedly insured), nearly half of them $2,000 or more. The authors remind us that most national studies of medical debt are based on reports from collection agencies and the actual level of debt is much higher - most debtors are still paying their providers directly. Healing and Stealing strongly recommends reading the full report.

However, you may want to skip the last two paragraphs, at least metaphorically. The report’s introduction and recommendations rely on the same “progress” narrative adopted by the Harris campaign. We’ve made “sweeping coverage gains” since the ACA’s passage, but “gaps” remain.

The United States has made considerable gains in health insurance coverage since the Affordable Care Act’s passage, but more work is needed to cover the remaining uninsured, eliminate gaps in coverage, and ensure that all health insurance does what it’s supposed to: enable people to get health care when it’s needed, without fear of incurring debt.

As is common with such reports, Commonwealth’s policy recommendations are inadequate to the problems they describe. The top of the list is maintaining the expanded ACA subsidies that will expire next year, the Harris campaign’s central health care promise. Allowing them to sunset would be a congressional act of casual cruelty, but the decline in the percentage of allegedly well-covered adults and rise in people skipping needed treatment over the past two years took place while the enhanced subsidies were in full effect.

Readers should evaluate them for themselves, but the rest of the recommendations are minor tweaks that only feel urgent if one accepts that we’ve made “considerable gains” and that the policy task is filling “gaps.” The focus is so narrow that the recommendations don’t even acknowledge the existence of California’s unified financing law or Oregon’s single-payer planning process, let alone analyze what portions might survive under a Trump Administration.

Oddly, the authors say that one option to expand coverage would be for Congress to create a back up federal plan to cover low-income adults in states that have refused to expand Medicaid. This has no more chance of passing a Republican Congress than Medicare for All, dropping the Medicare eligibility age to 50 or any other significant universal reform. Yet the authors avoid making the case for more effective but equally “unrealistic” change.

The report’s portrait of health care among working-age adults is an indictment of the failure of employer-sponsored insurance. Most adults between the ages of 19 and 64 who have any health insurance at all get it through their jobs. Sixty-six percent of the adults who meet the authors’ narrow definition of “underinsured” are covered by an employer plan.

The odds that the incoming Trump Administration will take policy action that actually helps employed U.S. adults cope with health care costs are infinitesimally tiny - a rounding error on a rounding error. Leaving aside horrific human suffering, as Healing and Stealing’s data showed, mass deportation would have a net negative effect on overall health care costs, since undocumented taxpayers subsidize health care for other U.S. residents.

Trump has abandoned his ambitious proposals to control prescription drug costs. His vague hints at offering lower cost health plans are likely a reference to longstanding Republican desires to allow the sale of even more bare-bones insurance plans to employers and individuals and further expand the use of high deductible plans, all of it snake oil. In the short run, GOP politicians might be able to film happy people whose premiums declined for campaign ads. Perhaps another decline in the technical rate of “uninsurance” will allow Republicans to launch their own delusional “progress” bandwagon.

In the end, expanding the sale of “insurance” with even higher out of pocket costs would likely just swell the ranks of the underinsured and allegedly well-insured that the Commonwealth Fund surveys every two years.